The Ascent

Own the Substrate — A Map to 2045

“The world is being repriced, rebuilt, and redrawn. Beneath it all is the Ascent.”

Preface

This is the paper I have wanted to write for a long time.

Most of what gets called analysis today is reaction. People watch a print, watch a chart, watch a headline, and try to extrapolate the next ninety days. That is not analysis, that is positioning.

What I am going to lay out here is a forecast for the road to 2045. The nearly two decades between now and then are going to compress more change into the human experience than any equivalent window in modern history. I say it because the math suggests it.

I am writing this as an investor. I am also writing it as someone who believes the most important thing a serious person can do right now is build a coherent picture of where this is going. Without that picture, everything looks like noise. With it, more of it looks like signal.

The thesis is simple. The implications are not.

We are living through what I am calling the Ascent: the simultaneous reorganization of every major system humans have built over the last five hundred years. Labor. Energy. Money. Empire. The boundary between Earth and space. The boundary between human cognition and machine cognition.

All of it is moving at once.

This is not the end of the world, but it is the end of a world. The next one is being built, in plain sight, by people who are not asking permission and are not waiting for consensus.

This paper is my attempt to map the structure of that next world, and to lay out the long-duration trades that follow from it.

Most pieces of this thesis exist elsewhere. AI labor displacement, the grid bottleneck, critical minerals, the space economy, defense modernization, dollar erosion, great-power competition. None of these are mine. What is mine is the integration and synthesis. The argument that all of these forces are stacked exponentials feeding the same transition, the framing of the National Security Stack as a single emerging entity, and the Redraw chapter on memetic warfare. The synthesis is the contribution.

I am writing this with conviction. The destination of this transition is, in my view, the most likely structural outcome. The most important debate is about pathing and speed. I should be clear that I started writing this paper already long the buildout. The reader should weigh the analysis with that bias visible rather than buried.

If you take only one thing away, take this: the people who reach 2045 in the right position will not be the ones who saw it coming. They will be the ones who acted while the rest were still arguing about whether it was real.

This paper is also the operating worldview behind my own investment practice. The mandate is straightforward: long-duration ownership of the substrate of what is emerging. The four frontiers are where the structural exposure lives: AI, robotics, energy, space, with defense as the envelope that runs across all of them. The job is to identify the bottlenecks, own the strategic assets, and hold through the volatility. Not to trade headlines.

The Core Claim

This paper is not the end of an argument. It is the source code for one.

The road to 2045 will shift wealth and power from those who sell labor or hold paper claims to those who own the infrastructure of automated production, energy abundance, and frontier expansion.

Human civilization is moving from a labor-constrained, energy-constrained, planet-bound economy into an intelligence-abundant, automation-heavy, energy-expanding, space-capable one. The transition will be volatile, politically destabilizing, and monetarily messy.

Compute, robotics, energy, launch costs, and synthetic biology are all inflecting at once. The curves feed each other. The buildout required to support them is one of the largest infrastructure cycles ever attempted. The grid, the supply chain, and the political system are not configured for it. Capital is flowing into the bottlenecks, and the companies and countries that own the means of automated production are going to capture a structural share of global output.

The Four Frontiers. AI. Robotics. Energy. Space. Defense is the envelope that runs across all four.

The Posture. Long-duration ownership, not short-term trading. Position for the decade. Hold through the drawdowns. Ignore the noise engineered to remove you from the position.

The analytical core of this paper covers the road to 2045. Some claims extend past that into what I call the mythic horizon. Those are not trades for today. They are the long arc the bottleneck decade makes possible.

First, I want you to feel the transition. Then I will give you the map.

Table of Contents

I. We Are Living Through It

II. The Comprehension Gap

III. The Repricing of Intelligence

IV. The Energy and Materials Reckoning

V. The Expansion Into Space

VI. The Erosion of Money

VII. After Unipolarity

VIII. The National Security Stack

IX. After Labor-Capitalism

X. The Coalition of Fear

XI. The Redraw of Reality

XII. The Ascent

XIII. The Bets

XIV. The Trade and the Hold

Signals to Watch

Selected Sources

Parting Thoughts

I. We Are Living Through It

You are not in a normal market cycle. You are not in a normal political cycle. You are not in a normal cultural cycle.

You are in a transition.

Transitions feel like collapse from the inside. That is the part nobody tells you. When you read about the Industrial Revolution in a textbook, it sounds clean. A diagram with arrows. Steam, then rail, then electricity. In real time, it was riots, panics, depressions, wars, displaced populations, broken families, and decades of confusion punctuated by sudden bursts of unrecognizable wealth. The people inside it had no idea what they were inside.

We have no idea what we are inside.

The shape of every major transition rhymes. The old systems do not die quickly. They centralize. They print money. They demand loyalty. They invent new enemies. They suppress the new thing as long as they can, and then, when they realize they cannot, they try to absorb it. Sometimes they succeed. Often they do not.

What is different this time is the speed. The Industrial Revolution unfolded over roughly a century and a half. The internet revolution unfolded over roughly thirty years. The current transition is going to unfold faster, because multiple curves are inflecting at the same moment. Compute. Algorithms. Robotics. Energy generation. Launch costs. Synthetic biology. Each one would be a generational shift on its own. They are arriving simultaneously, and they feed on each other.

This is what people miss when they argue about whether AI is overhyped. They are looking at one curve. The story is not one curve. The story is what happens when six curves intersect.

When you are inside an intersection like this, your job is not to be right about the next quarter. Your job is to position for the next decade and to stay grounded when the noise becomes deafening.

One thing the reader can verify without my help: look at where the talent is going. For fifteen years, the best engineers, the best mathematicians, and the best operators were building algorithmic trading systems, dopamine-optimized consumer apps, ad-tech machines, and increasingly elaborate financial instruments. They were rewarded for making attention more addictive and capital more leveraged. That is what the system asked for, and the system got it.

That is changing. The talent is leaving those industries and going into AI, robotics, energy, defense, hardware, and biology. People are leaving high-paying algorithmic seats for lower-paying lab seats because the work matters more. I am one of them. I operated in crypto from 2015 to 2025, and I still respect what is being built there. Agentic infrastructure rails, prediction markets, twenty-four-seven global derivatives. Real developments. But intellectually, the gravitational pull is elsewhere now. The center of mass of human ambition has shifted from financializing the world to building the next layer of civilization. The talent migration is one of the cleanest leading indicators in markets. Capital follows talent on a lag. Watch where it is going.

This is not a clean migration. Finance and crypto will still attract brilliant people because leverage, liquidity, and volatility always attract brilliant people. The point is not that all talent leaves financialization. The point is that the prestige frontier has moved.

The cycle we are inside of is much longer than most participants are pricing.

There will be a 2008-style event in the next decade. Maybe more than one. They are baked into a transition this large. In the long view, none of those events are the story. They are punctuation inside the story. Pull the chart back far enough and the 2008 crash, an event that felt like the end of the world for the people inside it, looks like a tight little dip on the way to a structural up-leg that has not stopped for nearly two decades. The next crash, whatever triggers it, will look the same in retrospect. A blip. A clearing event. A line that sets up the next chapter.

The actual move, the one I am writing this paper to describe, is going to dwarf any individual crash that happens along the way. The buildout is too large and the transformation is too deep for the volatility around it to be the main event.

The traders who get destroyed by the next crash will not be destroyed by the crash. They will be destroyed by mistaking the punctuation for the sentence.

Hold the long frame, or get shaken out of it.

The first thing you have to accept is that almost everything you were taught about how the world works is going to stop working. Not all at once. Not gracefully. But predictably. How humans earn a living, store value, project power, create and verify knowledge, and mediate reality itself is all about to change.

If you can see that, you can build a thesis. If you cannot, you are going to spend the road to 2045 confused and afraid.

I am going to try to help you see it.

The Map

Now you have felt the transition. Here is the structure of how I am going to walk through it.

The Causal Chain

Here is the chain. If this chain holds, the thesis holds. The rest of the paper is my attempt to show that these links are not abstract. They are already forming in the world around us.

Compute and algorithms make intelligence cheap.

Cheap intelligence automates mental labor.

Embodied intelligence automates physical labor.

Automation explodes demand for energy, compute, chips, materials, and grid infrastructure.

These bottlenecks become national security assets.

States duplicate the stack, increasing defense and industrial spending across rival blocs.

Labor loses bargaining power. Ownership becomes the central economic claim.

Money is debased as states manage debt, instability, and transition costs.

Capital flows toward scarce, productive, strategic assets.

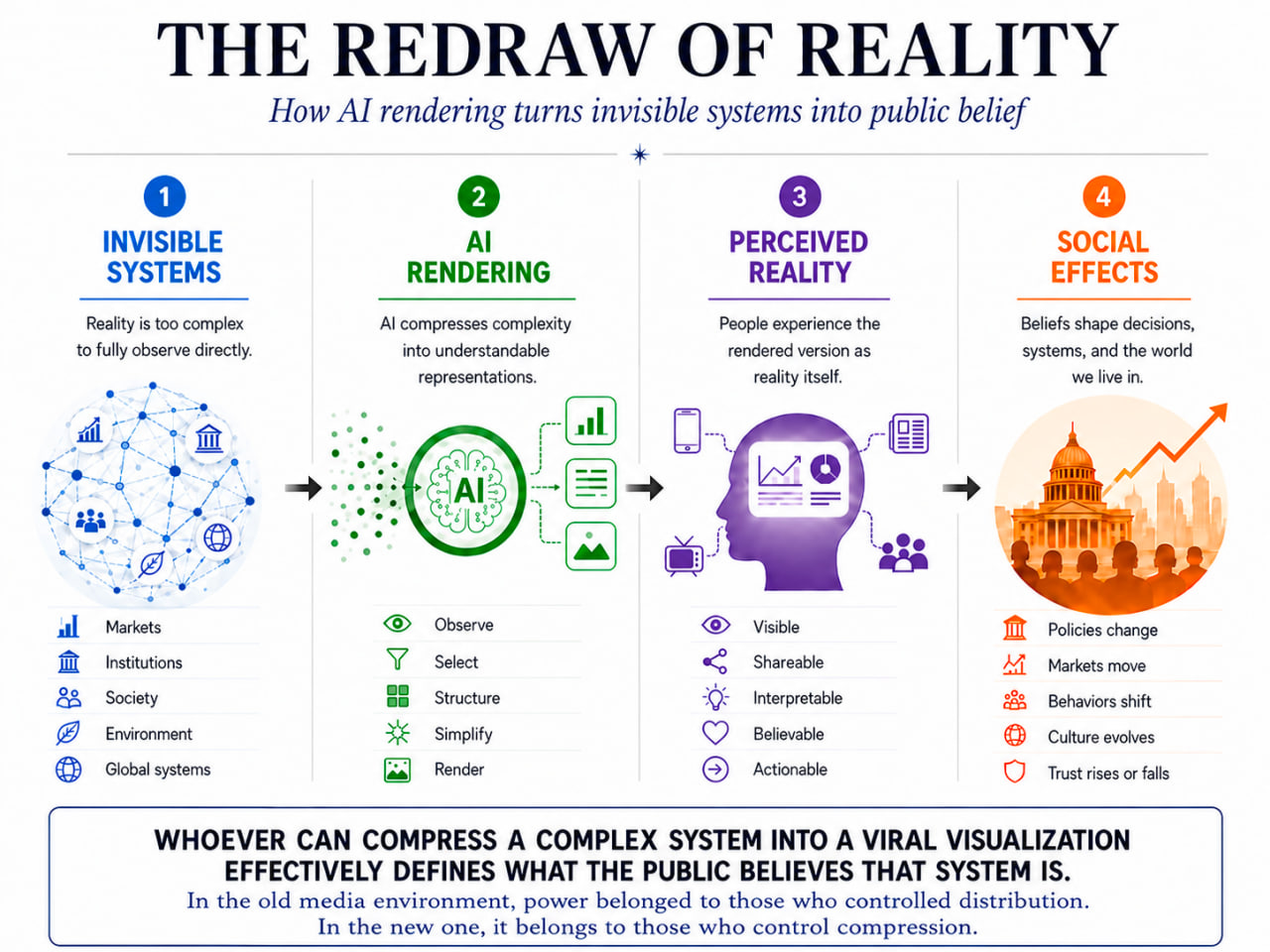

The visualization of complex systems, generated by AI, rewrites what ordinary humans perceive and accept as real.

Civilization expands outward. More energy. More intelligence. More automation. More space. More abundance.

The Core Concepts

These are the words I am going to keep using. Learn them once. They are the handles for the whole map.

The Ascent. Civilization’s shift out of scarcity: from human labor, limited energy, and a single planet toward abundant intelligence, automated production, expanding energy, and a presence beyond Earth. The whole document is a map of this shift.

The Four Frontiers. AI, robotics, energy, and space. These are the expansion frontiers. AI expands intelligence. Robotics expands labor. Energy expands power. Space expands territory. Defense is not a fifth frontier; it is the envelope, the state’s demand function running across all four, the form the frontiers take under national-security pressure. Biology is not on the list yet either; it is the inward turn of intelligence, and it enters the stack through the AI layer for now. Together the four frontiers form the National Security Stack.

Stacked Exponentials. Multiple compounding curves running simultaneously and feeding each other rather than progressing independently. The dynamics this produces have no clean historical analog. Linear minds processing them produce systematic underestimates that look reasonable until they suddenly look ridiculous.

The Bottleneck Decade. The roughly ten-to-fifteen year window in which energy, materials, grid, compute, and political systems lag behind technological demand. The window I am writing this paper inside of. The window where the trade is.

The Ownership Problem. The political and economic crisis created when labor loses bargaining power and ownership of automated systems becomes the dominant claim on output. Most of the political conflict ahead is going to be downstream of this.

Citizen Ownership. The broad category of mechanisms that give citizens some participation in the productivity of automated systems. This could take the form of sovereign wealth funds, birthright investment accounts, public equity stakes, tax-advantaged citizen portfolios, tokenized national equity, direct transfers, or some future structure we have not named yet. Universal Basic Equity is one possible version: a minimum civic stake in the productive base of the society a citizen belongs to. Not equal ownership. Not equal outcomes. A floor, not a ceiling. The important point is not the instrument. The important point is that a society where labor loses bargaining power needs some mechanism for broad participation in capital ownership.

The National Security Stack. AI, robotics, energy, space, and the critical materials underneath them are no longer normal sectors. They are state capability. Defense is the envelope around them, the form they take under national-security pressure, not a separate sector beside them. Once a company enters this envelope, it stops being priced like a normal business.

The Redraw of Reality. AI-generated visualization making previously invisible systems visible to ordinary humans, and memetically transmissible at the speed of the feed. A new telescope and microscope for public consciousness, with a corresponding propaganda surface. Whoever can compress a complex system into a viral visualization effectively defines what the public believes that system is.

The Coalition of Fear. The politically incoherent but emotionally coherent alliance of groups that oppose technological acceleration for incompatible reasons, with AI as the current symbol and easiest target: labor displacement, surveillance, religious and moral concern, institutional distrust, credential collapse, creative extraction, concentration of power, and fear of civilizational loss of control. Many of their concerns are real, and some of their critiques are coherent analytical positions rather than fear responses. The shared weakness across the coalition is that resistance has no shared alternative to the buildout.

The Hold. The behavioral discipline required to remain positioned through structural volatility. The actual alpha in this transition is not picking the trend, it is staying on it long enough for it to compound.

Mythic Horizon. The far edge of the thesis. Not trades for today. Not spreadsheet items. The long arc: orbital biospheres, longevity escape velocity, off-Earth cities, full Singularity dynamics. I name them honestly. I do not bury them in the analytical sections.

II. The Comprehension Gap

The single largest barrier to seeing any of this clearly is not lack of information. It is the architecture of your own mind.

The human brain was not built to comprehend exponential growth. We were built to track tigers, seasons, and gradual changes in a herd or a forest. Our entire intuition system runs on linear extrapolation, because for the entire evolutionary history of our species, linear extrapolation was good enough.

It is no longer good enough. The world we are walking into compounds. Compounding breaks human intuition in a specific, predictable, expensive way.

The famous version of this is the rice on the chessboard. One grain on the first square. Two on the second. Doubling every square. By the eighth square, you have 128 grains. Manageable. By the fortieth square, you have over a trillion. By the sixty-fourth, you have more rice than humans have produced in all of recorded history. The math is correct. The intuition is wrong. Almost nobody, including educated people, including investors, can hold that picture in their head.

This is why almost every major technology of the last century has been simultaneously overhyped in the short run and underestimated in the long run. The phenomenon has a name. Amara’s Law: we overestimate the impact of technology in the short run and underestimate the effect in the long run. Cars. Electricity. Computers. The internet. Mobile. AI. Each was dismissed as overhyped after its first peak of attention. Each then transformed the world far beyond what its original advocates predicted.

There are several technical laws that govern what is happening, and each one matters for an investable reason.

The Laws That Govern This

Moore’s Law. Functional AI compute per dollar keeps falling, even as classical transistor scaling slowed. Implication: the cost curve expands the market faster than near-term margin compression can absorb. Margin-compression scares are buying windows, not disconfirmation.

Wright’s Law. Cost falls predictably as cumulative production rises. Solar, batteries, and memory chips all rode it. Implication: humanoid robotics is next. The first ten thousand units will be expensive. The ten millionth will be cheap. Nobody is pricing that curve.

Jevons Paradox. Greater efficiency increases total consumption, not less. Implication: as intelligence gets cheaper, total demand for it explodes. The “AI commoditizes, margins collapse, bubble pops” thesis is wrong about the system even where it is right about specific products.

The Stack

Single curves are hard for human brains to track. The harder problem is that these curves do not run in isolation. They multiply.

Cheaper compute, applied to better algorithms, running on more efficient energy, produces more capable AI. More capable AI, embedded in better robotics, manufactured at scale on Wright’s Law cost curves, produces a labor force that compounds without payroll. That labor force, applied to building more compute, more energy, and more robots, accelerates every other curve. Each output becomes the input to the next round.

We are entering a regime of stacked exponentials. The dynamics have no clean historical analog, and linear intuition keeps producing estimates that feel sober right up until they look absurd.

That is the comprehension gap. It is also the asymmetric opportunity. The people who can hold the stacked-exponential picture in their head, even imperfectly, are going to be positioned for the structural moves while everyone else is debating whether the technology is overhyped.

The “overhyped” debate misses the point. Short horizons run hot. Long horizons run cold. Almost nobody can hold both of those statements in their head at the same time.

III. The Repricing of Intelligence

In 2020, frontier language models could already produce impressive prose, but they were unreliable novelties rather than dependable tools. In 2026, frontier models are scoring at or above expert level on graduate-level benchmarks across mathematics, biology, law, and medicine, including exams that were considered out of reach even three years ago. They are writing production code. They are running experiments. They are operating computers autonomously. They are coordinating with each other.

This did not happen because of one clever insight. It happened because a brutally simple recipe kept working: more compute, more data, better algorithms, applied iteratively. Every six months, the recipe scales. Every six months, capabilities jump.

The pattern is not mysterious anymore. And it is still being underestimated, because capability scaling is exponential and the human brain processes the world linearly.

Important distinction: model capability is not deployment. A model that wins a benchmark is not the same as a model that has been integrated into a workflow, regulated, insured, and trusted with real consequences. The first runs ahead of the second by years. Both are happening. The deployment lag is real and matters for the trade.

The capability trajectory is not subtle. Frontier models landing in 2027 and 2028 will be qualitatively different from today’s. They will do extended autonomous work over hours, days, and eventually weeks. They will take a vague human goal, decompose it, execute, hit obstacles, replan, and complete.

Think of each frontier model as a drop-in knowledge worker who never sleeps, never quits, costs orders of magnitude less than the human equivalent, and can be cloned a thousand times in parallel. One worker today. Thousands soon after. Eventually, millions of parallel agents operating against the same class of task.

That is a research engineer. That is a lawyer. That is an analyst. That is a software developer. That is a scientist.

Zoom in from the macro picture to the individual. In ten years, any person with internet access will be able to operate like a company, with a powerful AI team around them. Research, writing, coding, analysis, design, scheduling, accounting, legal review, customer service. Tasks that previously required teams or agencies become solo work, executed at scale. The reverse is also true. Enterprises will increasingly run on AI-native operating systems where humans set direction and the system executes. The unit of economic production is being redefined at both ends.

This is what some have started calling Software 3.0. The model is not an app you open. It is the operating system the apps run on. The chatbot was the first surface, the way the command line was the first surface for the personal computer, and it is just as misleading about where the value sits. The interface is not the thing. The substrate underneath it is the thing, and the substrate is compute, models, and energy.

This quietly breaks the logic that explains why companies exist at all. Firms formed because coordinating people inside an organization was cheaper than transacting for every task on the open market. When AI collapses the cost of execution and coordination, that logic weakens, and the smallest viable unit of serious economic production keeps shrinking.

You can argue about timelines. The direction is much harder to argue with.

The labs know this. The hyperscalers know this. The sovereigns know this. That is why hundred-billion-dollar capex commitments are being made in months instead of years. That is why nation-states are scrambling to build domestic compute. That is why the energy contracts being signed for AI training runs are larger than the entire grid load of mid-sized countries.

The repricing of intelligence is not just a thesis. It is an observable buildout. The cement is being poured, the chips fabricated, the transformers installed, the fiber laid. You can see the future being constructed in physical space if you know where to look.

The Repricing of Human Labor

The repricing has a shadow, and the shadow has a name. Human labor, as the foundational economic unit of civilization, is being repriced. Mental labor first. Physical labor second.

The first wave is already underway. It is invisible because it is not happening through layoffs. Yet. It is happening through hiring freezes, through silent productivity gains, through teams of three doing the work of teams of fifteen. Companies are not announcing “we replaced you with AI.” They are announcing “we are flat year over year on headcount” while revenue per employee climbs. They are announcing “we are more profitable per employee than ever.” They are announcing “we are deploying productivity analytics across the organization.” Same thing measured from different sides.

They are also building the dataset that finishes the job. Surveillance tools rolled out across employee workstations under the banner of “productivity analytics” capture the workflows, decisions, and outputs that future models will be trained on. Workers are being monitored not to make them more efficient. They are being monitored to make their replacements possible.

Watch the entry-level job market. The bottom rung of the corporate ladder is being sawed off in software, law, finance, consulting, design, marketing, and research. Not because young people are lazy or unskilled. Because the work that used to be junior work is now done by a model in eleven seconds for two cents.

This is the leading indicator. The wave moves up the skill curve from there.

The second wave is robotics, and it has not started yet at scale. The bottleneck has never been the body. It has been the brain inside the body. The body has existed for years. The actuators, the sensors, the batteries, the kinematics. The hard part was getting a machine to look at a messy, unscripted, real-world environment and act in it precisely. That problem is now being solved by the same models that are eating mental labor, ported into bodies.

When you understand that, you understand why the same people who are betting tens of billions on AGI are also betting tens of billions on humanoid robotics. They are not separate trades. They are the same trade with two outputs.

Over the next decade, humanoid robots move from demos and pilots into real commercial work: warehouses first, then factories, construction, and logistics, then the harder service environments. The deployment curve inflects sometime in the 2030s. Most observers are modeling linear adoption; the actual path is closer to exponential, and the gap between those two curves is where the mispricing lives. By the time the Bottleneck Decade closes, the “human labor versus machine labor” question will be settled across many physical domains, and the economically interesting question becomes how the productivity gets distributed.

That last question is everything.

Robotics is the frontier where I am most likely to be early. The direction is obvious; the timing is not. Software scales instantly. Hardware does not. Actuators, batteries, safety cases, manufacturing yield, and reliability in unstructured environments all gate the curve. If this thesis is early anywhere, it is here. I expect to be wrong on timing before I am wrong on direction.

The death of human labor is not the death of human meaning. Those are two separate questions, and the people who conflate them are going to make terrible policy. The question is not whether humans will have purpose. The question is what economic and political arrangement we settle on while we figure out the next chapter.

But repricing is not uniform, and this is the part most automation commentary misses. The same tools that erase the value of average work multiply the value of exceptional work. A great engineer with AI is not 20% better than before. They are operating at a level that previously required an entire team. A great analyst, a great founder, a great researcher, a great operator: each one, paired with these systems, produces at a scale that had no precedent. The curve does not flatten. It bends into a K. The bottom and the middle of many fields get compressed while the top breaks away to levels of output and leverage that were physically impossible a decade ago. Same tools. Opposite outcomes, depending on which end of the curve you are on. The leverage is the largest it has ever been for the people who can wield it, and the smallest it has ever been for the people who cannot.

The fight over distribution is going to be brutal. It will look like culture war. It will look like class war. It will look like generational war. Underneath all of those surface fights, the real fight is about how to distribute the output of a civilization that no longer needs most of its citizens to produce its goods and services. That is the deep current. Every political conflict on the road to 2045 is going to be downstream of it.

The Third Repricing: Biology

There is a third repricing that belongs in this chapter, and it is large enough that readers may be tempted to treat it as a fifth frontier. Not yet. Biology is not a separate pillar beside the four frontiers today. It is the inward turn of intelligence: the same frontier, pointed at life itself rather than at silicon. For now it enters the stack through the AI layer. Most market participants are still treating it as venture-stage speculation. They are wrong.

Intelligence is being repriced through AI. Physical labor is being repriced through robotics. Biology itself is being repriced through the application of AI to the molecular and cellular layer. The third repricing is happening on the same curves as the first two, and it is going to be every bit as consequential.

For a hundred years, drug discovery has run on brutal economics: roughly a billion dollars and ten to fifteen years per approved drug, most candidates failing along the way. The bottleneck was never chemistry. It was the combinatorial search space, too many possible molecules and targets, too few experimental cycles per year. AI is collapsing that bottleneck.

Protein structure prediction is largely solved for most single proteins. The overwhelming majority of meaningful proteins, including ones never crystallized in a lab, can now be modeled to working accuracy in minutes, and the same models are learning to predict function, interaction, and small-molecule binding. The discovery loop is compressing from years to months to weeks. Automated end-to-end labs are turning what took a team of fifty PhDs into closed-loop systems that generate candidates, test them, learn, and iterate without human bottlenecks.

The categories that follow from this are real, near-term, and underpriced.

Drug discovery acceleration. AI-native pharma is bringing candidates into trials faster, with better target selection than legacy pharma. The track record is still short, but the economics of the whole industry are being rewritten regardless.

Aging biology and cellular reprogramming. The science of why cells age, and how to reset them, has moved from speculation to a real engineering discipline in the last five years, with the first interventions already in early clinical trials. My aggressive case is that early wealthy access arrives within a decade, with broader developed-world access within a generation.

Gene editing at scale. CRISPR has moved from one-off proofs of concept to a real pipeline. The first FDA-approved CRISPR therapy treats sickle cell; the next wave treats a long list of genetic conditions, and after that, broader applications including age-related disease.

Synthetic biology as a manufacturing platform. Engineered organisms producing materials, fuels, food, and pharmaceuticals at lower cost than petrochemical or agricultural processes. This is industrial chemistry running on biology rather than against it.

The market is treating most of this as speculative. The buildout is real. The capital is flowing. The talent migration into biotech-AI is one of the cleanest leading indicators in the field. By the time the Bottleneck Decade closes, biology will be one of the largest categories of repricing in the economy, alongside AI and robotics. Most observers will look back at the late 2020s and say it was obvious. It is not yet obvious. That is the trade.

Alpha: the AI-bio interface is the unlock for the next decade of medical fortunes. Some of it captured by legacy pharma entrenching its position. Some by AI-native challengers. Some by entirely new categories emerging from breakthroughs we cannot yet name. The winners will be whoever integrates machine learning into discovery and trials deepest. Bet on the integration, not the company type.

The Market Read

The companies and countries that build the means of automated production are going to capture a much larger share of total economic output than is currently priced. The companies and countries that fail to build them are going to be reduced to economic dependencies. The gap between the two will be enormous.

A note on evaluating the model layer itself. The right way to assess AI labs is not raw capability. It is the tradeoff between intelligence and cost. A model that is marginally smarter at ten times the price loses to one that is nearly as smart at a fraction of the cost. The leaders on this curve rotate faster than most observers track. A lab that dominates the intelligence-per-dollar frontier one quarter can fall off it the next when a competitor makes a sharper architectural bet. This is why “who is winning AI” is the wrong question. The question is who sits on the cost-adjusted frontier right now, and that answer keeps changing.

You either own the machines, or you do not. That is the trade.

Alpha: own the substrate, not the application layer. Compute, energy, and chip architectures capture the value the application layer competes away.

IV. The Energy and Materials Reckoning

You cannot run intelligence at this scale on the current grid. You cannot run robotic civilization on the current grid. You cannot run space industrialization on the current grid.

The grid was built for a world that no longer exists. The world we are walking into needs significantly more power, distributed differently, generated differently, and built faster than current permitting and construction timelines allow.

This is not opinion. It is arithmetic.

That is why I am not merely bullish on energy companies. I am bullish on energy expansion itself. The market is obsessed with the intelligence layer. I think the true choke point this decade is the physical layer underneath it: electrons on the wire, uranium in the ground, gas in the turbine, copper in the cable, transformers in the yard, and interconnection agreements in the queue. Software compounds at the speed of deployment. Power compounds at the speed of steel, concrete, mines, substations, and public approval. That mismatch is the trade.

The IEA projects global data center electricity consumption rising from roughly 415 TWh in 2024 to around 945 TWh by 2030, more than doubling in six years. In the United States, data centers account for nearly half of projected electricity demand growth between now and 2030. This is not a normal load-growth cycle. This is a new industrial demand curve landing on a grid built for a slower world.

The supply side cannot follow cleanly. Berkeley Lab’s latest interconnection data shows more than 2,060 gigawatts of generation and storage capacity actively seeking U.S. grid connection as of the end of 2025. The 2025 edition showed roughly 10,300 active projects in the queue at the end of 2024, representing 1,400 GW of generation and about 890 GW of storage. Most projects that enter interconnection queues are withdrawn, and the ones that get built are taking longer to move from request to operation.

The bottleneck is not just megawatts. It is hardware. Large power transformer lead times now average roughly 128 weeks, with generator step-up transformers running around 143 to 144 weeks. The United States remains heavily exposed to imported transformer supply at the exact moment AI, electrification, renewables, and grid replacement are all pulling on the same equipment stack.

The hard version of the claim is this: if the energy buildout does not arrive on the AI buildout’s timeline, the AI buildout itself stalls. Not because the algorithms fail. Because the power does not show up. Google has already identified the U.S. transmission system as the biggest challenge to connecting data centers, with grid connection delays reaching up to twelve years in some regions. Hyperscalers are responding by contracting power directly, colocating near generation, building or exploring on-site power, and treating time to power as the binding constraint on revenue rather than chip procurement.

So we are going to build everything. Nuclear is back, real nuclear, not just SMRs. The first new full-scale fission plants built in the United States in decades have come online. Politicians who would have lost their careers for supporting nuclear ten years ago are leading the charge. It is hard to see a full AI buildout without significant nuclear. Natural gas is the ugly bridge. It is not the final answer, but it will carry more of the Bottleneck Decade than clean-energy purists want to admit. Solar and wind scale but cannot carry industrial-grade base load. Geothermal could become a bigger story than current consensus assumes. Fusion is coming, and when it arrives at scale, it changes the price of everything.

But the bottleneck is not generation. The bottleneck is the physical inputs.

To build the grid required for the next twenty years, you need staggering quantities of copper, steel, aluminum, lithium, uranium, rare earths, silver, nickel, and cobalt. The mines that would produce these materials in the volumes required have not been built. Some have not been permitted. The IEA projects a roughly 30% copper supply deficit by 2035 under current pipelines. New copper projects take about 17 years from discovery to production. Most rare earths processing capacity is currently in China.

We are about to spend a decade trying to build a 2050 grid with a 1990 supply chain.

Uranium deserves its own treatment. Demand is inflecting from both sides. AI is the largest new electricity demand in modern history, and the only baseload that scales without hydrocarbons is fission. Supply is structurally constrained. Processing capacity sits in jurisdictions the West cannot rely on. New mines take a decade. The uranium trade is the single cleanest expression of the AI buildout meeting the energy bottleneck.

This is where energy stops being a market story and becomes a security story.

The countries that lock up copper, uranium, rare earths, processing capacity, and grid hardware win the buildout. The countries that do not become dependent. We are already in the early phase of the resource wars. Not always with armies. More often with financing, proxies, mercenary companies, export controls, basing rights, drone coverage, and quiet mineral contracts being signed in ways that mostly do not appear on television. By the mid-2030s, this will be one of the dominant security frames in the world.

The dominos are sequenced. AI improves the math models that improve materials science. Better materials science unlocks better batteries, better superconductors, better solar, better grid hardware, and eventually working fusion. Better energy makes more AI possible. The loop closes. Each round of the loop is shorter than the last. Researchers who have lived through five-year discovery cycles in materials are watching the same work happen in months. The same domino chain runs through biology, chemistry, and structural engineering. The cascade is what makes the bottleneck decade end. It is also what makes the post-bottleneck decade look nothing like the current one.

The price implications are obvious. Hard commodities, especially the ones that are critical and supply-constrained, are going to experience a structural bull market that lasts until either supply catches up or demand collapses. Neither is happening on the current trajectory. Copper, uranium, and gold are not trades. They are positions you hold for the decade.

There is a second-order effect worth understanding. In a genuine supply shortage, the lowest-quality producers reprice the hardest. The high-cost marginal supplier that was near bankruptcy when supply was loose becomes a cash machine when demand outruns capacity. This is standard commodity-cycle behavior, and the energy and grid buildout will follow it. The cleanest assets compound steadily. The marginal, high-cost, previously-uneconomic capacity moves violently when the shortage hits. Both are part of the trade. Understand which one you are holding, because the violent movers are rentals, not homes.

Beyond the commodities, the second-order trade is the energy infrastructure itself: transmission, transformers, switchgear, cooling, storage. The boring physical layer of the grid is suddenly strategic. Companies that make these things are sitting on multi-decade backlogs and pricing power they have not had since the 1960s.

This is also the sector where you see the most unambiguous signal that government and capital are aligned. Industrial policy is back. Subsidies are flowing. Reshoring is happening. When both parties suddenly agree on power, grid security, and minerals, pay attention. They have seen the same numbers.

The numbers are: build, or fall behind permanently. We are going to build.

Alpha: the scarce inputs to the buildout are scarcer than the buildout itself. Copper, uranium, rare earths, grid interconnection, and processing capacity outperform the equipment built on top of them.

V. The Expansion Into Space

For most of the first space age, space was state-led, state-funded, and state-gated. That changed when reusable launch turned access to orbit from a government program into an industrial cost curve. What comes next is a frontier in the historical sense of the word: a place where civilization expands, settles, and extracts.

There is a deeper frame underneath all of this. The Kardashev scale, first proposed by Soviet astrophysicist Nikolai Kardashev in 1964 and revived in the current tech conversation by Musk, classifies civilizations by how much energy they harness. We are still below Type I: a civilization that has not yet fully captured the usable energy of its home planet. Climbing further requires expanding the energy budget, and the path to capturing stellar-scale energy eventually runs through space.

This is where two of the frontiers stop being separate. The ultimate energy opportunity and the ultimate space opportunity are the same opportunity. The sun radiates more energy in an hour than civilization uses in a year, and almost all of it misses the Earth entirely, streaming past us into empty space. A civilization that wants to keep expanding its energy budget eventually stops fighting over the sliver that reaches the ground and goes to where the energy actually is. Energy becomes a space problem, and space becomes an energy story. The near-term expression is terrestrial; the bottleneck decade is fought on the grid, with uranium and copper and transformers. But the direction of travel, across a long enough horizon, points off-planet, and the same launch and orbital-infrastructure layer the rest of the space thesis depends on is what eventually makes it reachable.

Reusability collapsed launch costs by an order of magnitude in less than a decade. Another order of magnitude is coming. Compress the cost of access to orbit by two orders of magnitude and you do not get a slightly bigger space industry. You get an entirely new physics of what is economically viable.

There is a second accelerant beneath the cost curve, and it is the same one driving the rest of this paper. AI is compressing the physics and materials loop that space hardware runs on. The same models accelerating drug discovery and materials science are being pointed at the hard engineering problems of getting to orbit and operating there: lighter and more heat-tolerant alloys, better combustion and propulsion modeling, faster simulation of launch, reentry, and orbital mechanics that used to eat years of compute and wind-tunnel time. This is not AI discovering new physics, it is AI collapsing the cycle time on the applied physics and engineering we already know, the same way it is collapsing the discovery cycle everywhere else. Every turn of that loop makes the hardware cheaper, lighter, and more reliable, which bends the launch cost curve faster than rocketry alone would. The space frontier is accelerating partly because the intelligence frontier is feeding it.

By 2040, the space economy will include categories that are barely investable today: orbital manufacturing, lunar logistics, in-space resources, space-based defense, and settlement infrastructure. Some of these have already started to attract serious capital. Orbital compute is no longer hypothetical. Others are still a decade from being real businesses. The internet looked the same in 1998. The substrate fills in. Then the substrate gets used in ways the original mappers could not see.

Launch is the toll road. The whole space economy sits on top of cheap, reliable, high-cadence access to orbit. Whoever owns the launch layer prices everything above them in the stack. The current structure of the market makes the point: one provider has driven cost-per-kilogram down by an order of magnitude and now runs the majority of global launch cadence, which is exactly why it is treated by the state as strategic infrastructure and priced by the commercial market it dominates. After launch, the most valuable layer is constellations: communications, earth observation, positioning, weather, defense, surveillance, and applications nobody has invented yet. The orbital infrastructure layer will be more valuable than terrestrial telecom infrastructure ever was.

Beyond infrastructure, the next layer is manufacturing and resources. Microgravity changes physics. Some materials are dramatically better made in orbit. The category moves from curiosity to real sector as launch costs fall. Asteroid resources are a longer-duration story: platinum group metals, water, and rare earths in volumes that dwarf Earth’s reserves. The economics of bringing them down do not work yet. The economics of using them in orbit work much sooner. Water in orbit means fuel in orbit. Fuel in orbit opens the solar system.

Orbital compute. As launch costs collapse, orbital data centers are becoming a serious candidate for the outer edge of the compute stack. The advantages: continuous solar exposure, passive cooling, no permitting fights, no zoning battles, no water disputes. The bottlenecks: launch cadence, on-orbit maintenance, harsh-environment engineering, latency, bandwidth. Most of these are real constraints right now. None of them survive the long run. The Starship cost curve is what makes the math work. The space substrate seems inevitable to me. The only real question is timing. The Bottleneck Decade does not depend on orbital compute being right; it is upside on top of a thesis that stands without it.

Space is now a war-fighting domain, and every serious nation knows it. The investment flow is following. Settlement of the moon and Mars is slow, expensive, and dramatic. Mythic horizon: eventually, there will be early cities.

Launch capacity is national security infrastructure. Orbital compute is downstream of the energy and compute thesis. Asteroid resources are the hundred-year answer to the materials bottleneck. The companies that own meaningful pieces of the space stack are likely to capture wealth at a scale the market is not yet built to price. Where the largest pools of private and public capital are already flowing is a tell about where the next century goes.

Humans expanding off-planet is not a side effect of technology. It is what life does. Single-celled organisms colonized the oceans. Then the land. Then the air. Consciousness keeps reaching outward. We are crossing from a one-planet species to a multi-planet one.

People who feel that will be drawn to the space trade in a way that has nothing to do with quarterly earnings. People who do not will misprice it. The mispricing is the opportunity.

VI. The Erosion of Money

The dollar, as you have known it, is changing. Not in whether it remains globally dominant. In whether it remains a stable long-duration store of purchasing power. It is not going to disappear. It is going to slowly transform into something more managed, more debased, and ultimately a unit of political power rather than a stable store of value.

This is not a crash thesis. It is a slow-motion thesis. The mechanism is structural.

The United States now carries approximately $39 trillion of federal debt. The math on servicing it does not balance through cuts or taxes alone. Not at current interest rates. Not under current entitlement obligations. Not given current defense commitments or demographic trends. It balances through some combination of growth, financial repression, and inflation. Politically, inflation is the path of least resistance, which is why it tends to do the heaviest lifting. The debate is not whether the fiscal path is strained. The debate is how long markets will tolerate it, and which mechanisms absorb the imbalance.

The obvious objection is U.S. exceptionalism, and it is real. Deep markets, dollar inertia, the strongest alliance structure, and AI-driven productivity could all extend the fiscal runway. That is why this is not a dollar-collapse thesis. It is an erosion thesis. The dollar can remain dominant while becoming a worse long-duration store of purchasing power.

“The Fed is going to keep printing” is too imprecise. The mechanisms are several:

Direct balance sheet expansion through QE in response to crises.

Tolerance of inflation above the 2% target for extended periods.

Emergency lending facilities that backstop specific sectors (banking, money markets, repo).

Implicit accommodation of fiscal deficits through Treasury market interventions.

Regulatory changes that encourage banks and insurers to absorb sovereign debt.

These are not equally likely in any given crisis. The pattern is that whichever lever is politically available gets pulled, and the result on long-duration purchasing power is similar regardless of which mechanism. The Fed balance sheet stood at roughly $6.7 trillion as of April 2026. The point is the direction, not the date.

What does break look like? A bank failure, a sovereign auction that does not clear, a credit market freezing, a foreign holder dumping treasuries. The specific trigger does not matter. The response will. More liquidity, lower rates, larger balance sheet, longer than anyone expected, deeper than anyone forecast.

Large corporations want the machine to keep running. Monetary stimulus disproportionately flows to the most leveraged, most politically connected companies. Their cost of capital collapses, their lobbyists get bigger budgets, and the next round of stimulus arrives faster. The bailout machine is a permanent feature. Every bailout makes the next one more likely. The public balance sheet has no hard limit, only a soft one called inflation, crossed gradually and then suddenly.

Here is the part of this argument I have not seen made clearly elsewhere. The AI buildout itself increases the probability of financial repression in a way previous cycles did not.

Look at the capex required. Stargate-scale data centers. Grid expansion. Critical mineral processing onshored at any cost. Every one of these is too large for normal capital allocation, too strategic to lose, and too slow to wait for organic returns. They get underwritten by the state.

When required capex exceeds what private markets can fund on commercial terms AND the assets are deemed strategically essential, the state underwrites them. Not always through direct spending. Often through guarantees, yield suppression, regulatory capital treatment, emergency facilities, and balance-sheet expansion. The AI cycle is the first where capex requirements collide with fiscal limits at the moment geopolitical stakes make withdrawal impossible. That collision produces structural debasement. The buildout cannot be lost.

The implication is direct: if you want to preserve and grow real wealth across the next twenty years, you cannot trust the unit of measurement. You have to own things that cannot be printed. Hard assets. Productive assets. Scarce assets.

Gold has been doing its job quietly for five thousand years. That is the Lindy effect made literal: the longer something has survived, the longer it is likely to keep surviving. Five thousand years of monetary status is data. Eighty years of dollar reserve status is hypothesis. Central banks know this. They are buying it at historically elevated levels, broadly distributed across countries. Gold itself has roughly doubled since 2023. The bigger signal is structural: per World Gold Council data, marked to market, foreign official gold holdings surpassed foreign official holdings of U.S. Treasuries in late 2025, the first time since 1996. When the people who run the printing presses are quietly buying the thing that cannot be printed, you should pay attention.

Equities of companies that own real productive capacity, that operate the infrastructure of the future, that generate cash flows that can grow with or beat inflation. These are not safe in the short term. They are essential in the long term.

Real estate in places growing demographically and economically.

What you cannot afford to own, on a twenty-year horizon, is large amounts of long-duration sovereign debt at current yields, denominated in currencies that are going to be debased to manage that same debt. That is the trap that pension funds, insurance companies, and conservative retail investors are sitting in right now, and most of them do not realize it.

The erosion of money is not a crash. It is a grind. The grind redistributes wealth from holders of paper claims to holders of real things. The redistribution is going to be one of the largest in modern history. It is already underway. You can either be on the right side of it or the wrong side of it.

Lindy is not just a monetary heuristic. It is a survival pattern that applies to anything humans carry across generations. Religions, brands, languages, recipes, institutions. What survives gets more durable the longer it survives. It is the meme nature of human civilization itself. The old becomes harder to replace the older it gets.

Alpha: hard assets, productive ownership, multiple income streams, low single-source dependencies. The dollar is not collapsing. Its purchasing power over real things is.

VII. After Unipolarity

Empires do not collapse cleanly. They transition. They do it badly, expensively, and over decades.

The American empire constructed after 1945 is in transition. That sentence will get read as alarmist or anti-American depending on who is reading it. It is neither. It is structural.

The Pax Americana was built on overwhelming military superiority, dollar hegemony, manufacturing dominance, energy depth, demographic vitality, institutional trust, and cultural confidence. Most have weakened. None are unchallenged.

China is the central competitor, and it is in a category of its own: the only nation able to contest the United States across every domain at once. Manufacturing, AI, energy, space, defense, and the industrial base underneath all of them. It is not a regional power testing the edges of American influence. It is a peer building a complete alternative to the American-led order, and the competition with it will define the geopolitics of the next several decades. The deep structure of the next era is bipolar: two poles, the United States and China, each anchoring a technological, financial, and military sphere. Everyone else is consequential but not co-equal. India, the Gulf, Brazil, and the rest are the contested middle, hedging between the two poles, building leverage by refusing to fully commit to either. The reorganization of South-South trade and the slow construction of payment rails outside the dollar system are real, but they resolve into which pole a given country leans toward, not into a world of many independent centers.

This is not American collapse. The U.S. is still the most innovative economy, the most militarily capable nation, the most attractive destination for global capital, with the deepest financial markets, most dynamic startup ecosystem, and largest reserve of soft power. None of that is going away in the next twenty years.

What is going away is the unipolar moment. The post-Cold War assumption that American norms, American institutions, and American currency would continue to set the global default. That assumption has been dying for a decade.

The transition is going to be expensive, and the expense will fall heavily on defense. You cannot maintain the obligations of the post-1945 order on the budgets of the post-1990 peace dividend. Funding levels are going up. Significantly. Permanently. Defense spending is no longer a political variable. It is a structural one, with bipartisan support that strengthens every year as the geopolitical environment hardens.

What the defense spending funds is also changing. The 2020s proved a new generation of capability in Ukraine: software-first, drone-first, autonomy-first, attritable, manufacturable at scale. The 2030s capture the procurement budget. The 2040s dominate. The next chapter is dedicated to that integration.

There is a deeper point here, which is that geopolitical fragmentation is driving duplication. China is building a parallel stack. India is building a parallel stack. Europe is building a parallel stack, finally. The Gulf is building its own stack with help from whoever will sell it. Every major power is now duplicating the entire technology pyramid: chips, AI, energy, space, defense.

That duplication is enormously expensive. It is also enormously stimulative. The companies that supply the duplication are going to do extraordinarily well. The geopolitical dynamic that forces the duplication is permanent. The unipolar moment is over. The duplicated world is the new normal.

For most of the post-Cold War era, frontier technology in the West treated itself as politically neutral. Customers were agnostic. Defense work was a stain rather than a duty. That posture worked when the West was the only game in town. It does not work now.

Competitors are not impressed by Silicon Valley’s pacifism. They are exploiting it. China has built a fully integrated state-industrial-military complex around AI, robotics, surveillance, and weapons. They have not debated whether technology should serve national interests. They have assumed it does and built accordingly.

The companies that figure this out early will be in a category of their own. The ones that are still posturing about whether to take defense contracts in 2030 will look like the ones who refused to take internet contracts in 1995.

VIII. The National Security Stack

The line between “civilian technology company” and “national security asset” is dissolving. In real time, on the timelines that matter now.

A data center that trains frontier models is national security infrastructure. A factory that produces humanoid robots is national security infrastructure. A chip fab, a uranium enrichment facility, a rocket launch facility, a rare earth processing line. All of it. The buildout now underway is not happening alongside national security policy. It is becoming national security policy.

This is the National Security Stack. It is the integrated set of frontier industries that nation-states now treat as strategic assets rather than commercial sectors. The four frontiers of this buildout (AI, robotics, energy, space) are not separate sectors that happen to be growing. They are pieces of a single national capability stack, and serious states are organizing themselves to control as much of that stack as they can.

You may notice defense is not on the list, because it is not a frontier; it is the envelope. It is what the other four become under pressure, the state’s demand function running across all of them. A drone maker is robotics with a government customer. A launch provider is space with a clearance. There is no defense sector in this framework. There is the stack, and the share of it the state claims.

Biology is not on the list either. It is coming. For now, bio enters the stack through the AI layer: every frontier lab already treats biological capability as a weapons question, and the policy apparatus is beginning to agree. But the four frontiers above are defined by physical buildout the state can fund, fence, and defend. When governments start buying biological capability the way they buy launch, the stack gets a fifth pillar.

What It Looks Like

Data centers are going to be hardened, defended, and in some cases physically protected by uniformed personnel. The new clusters are critical infrastructure under multiple legal frameworks, and the operational security requirements will reflect that.

Robot factories are going to be subject to export controls, security clearances, and protected status under critical infrastructure law. The companies producing humanoid platforms at scale will find themselves negotiating with defense ministries the way semiconductor companies negotiate today.

AI models above a certain capability threshold are already treated like weapons systems for purposes of export, deployment, and ownership. Washington decides which chips cross which borders, and in 2025 it began taking a cut: the two leading AI chipmakers agreed to hand the US government 15% of their China chip revenue in exchange for export licenses. A state toll on the outbound flow of strategic capability.

Energy infrastructure that supports the buildout (nuclear plants, enrichment, transmission, critical commodity supply) is being subsidized, fast-tracked, and strategically directed. Several G7 governments are implementing forms of intervention in their domestic energy stacks that would have been unthinkable a decade ago.

Space infrastructure is already partly classified. It is becoming more so. Launch capacity, orbital sensing, satellite communications, and lunar logistics will operate inside frameworks that look more like the defense industrial base than the commercial telecom industry.

Critical materials are the stack’s most concentrated national-security exposure. Copper, lithium, rare earths, tungsten, antimony, gallium, germanium. China largely controls the processing for all of them, and Beijing has stopped pretending otherwise: an outright ban on gallium, germanium, and antimony exports to the US in late 2024, then rare earth and magnet controls in April 2025 that froze Western auto lines within weeks, then another tightening in October. These metals are in the missile, the radar, the magnet, the night-vision optic, the engine. An entire generation of Western defense systems runs on a supply chain the West does not control. The reshoring is happening, expensively and with heavy subsidy. The companies building the alternative supply chain are not just being supported. They are being underwritten.

Who Sets the Price

The companies building the stack are going to have government in the room: intelligence liaisons, export rules, security obligations, national-interest constraints that 2010s tech companies would have considered insane. The ones that resist will lose contracts and access. The ones that embrace the integration will gain protection, capital, and structural advantage that nobody outside the security frame can compete with. But state protection is not free. The same designation that brings subsidy, contracts, and capital access also brings price controls, forced domestic sourcing, export restrictions, political oversight, and eventually nationalization risk. Strategic asset status is a moat and a leash.

So which one dominates? The defense primes have held strategic status for seventy years, and it bought them cost-plus contracts, single-digit margins, and returns that came from buybacks rather than growth. If “the government will defend it” were sufficient, Lockheed would have been the trade of the century. It was not. Protected and owned is not a growth story. It is a coupon.

The variable that separates the winners from the hostages is who owns the demand curve.

If the government is your only customer, the leash dominates. You get the moat, and with it a margin cap, procurement politics, and an upside that belongs to the taxpayer. You become infrastructure with a share price.

If the government protects you while commercial markets set your prices, the moat dominates. TSMC is subsidized, defended, and treated by two superpowers as the most important physical asset on earth, and its prices are set by commercial customers bidding for scarce leading-edge capacity. SpaceX is anchored by national security launch and priced by a commercial market it dominates. That is the position: the state guards the gate, the market sets the toll.

The best structure in the stack is the hybrid, the MP Materials deal. A government floor under the downside, commercial demand stacked on top. The state de-risks the capex. The market prices the output. Heads you compound. Tails the Pentagon owns your risk.

The equity itself is the tell. Washington is no longer just subsidizing the stack. It is buying it. The Pentagon on MP’s cap table. Stakes in the lithium and Alaskan copper developers. A golden share written into the US Steel acquisition. The state is assembling a portfolio of the assets it intends to keep, and a state does not let its own book fail. A government stake is the designation made explicit: that company will be defended, subsidized, and utilized, because the taxpayer is now long. The holdings are a published watchlist. But a stake does not change who owns the demand curve. It changes who absorbs the downside.

Intel is the live test of the framework. The state took 10% of a company the market had written off, and the stake alone settles nothing: a backstop under a melting business is still a melting business. Watch what stacked on top. SoftBank put in two billion. Nvidia followed with five billion and a chip partnership within weeks of Washington moving. The deal terms are even built to keep the foundry majority American-owned. What is still missing is the MP move: steered demand. The day Washington starts directing volume to the last American-owned leading-edge fab, this becomes the hybrid at semiconductor scale. That is the long-term bull case, and note what it bets on: the state finishing what it started.

When you look at any company inside the envelope, ask one question: who sets the price? If the answer is a procurement office, you are buying a bond with political risk attached. If the answer is a market, while the state guards the moat, you are looking at the most defensible equity on earth.

The End of the Biological Soldier

One piece deserves its own name.

The era in which the biological soldier is the default unit of deployment is ending. Not all at once, not cleanly, and not everywhere. But the procurement curve is moving away from humans as the first deployed unit and toward drones, autonomous systems, sensors, and robotic persistence. Ukraine settled the argument: small drones now account for the majority of battlefield casualties, and both sides build them by the million per year. Western procurement is reorganizing around that fact. The same humanoid and drone platforms being scaled for warehouses and factories are being scaled, in different versions, for these operations.

Alongside that shift, governments are going to converge on mass surveillance as the operating model in zones where they want to control resources or contain unrest. Drones overhead. Sensors on the ground. Persistent monitoring of populations and movements, executed by systems that do not need to sleep, eat, or be rotated home. This will be presented as security. It will also be the largest expansion of state observation capacity in human history, and it will land first in the places governments care about most: where the minerals are, where the supply lines run, and where the people are restive.

I am not endorsing this. I am telling you it is happening, and that the companies building these capabilities will be among the most valuable strategic assets of the coming decade. Every previous expansion of the military-industrial base has produced both real productive spillover and real destructive consequences. This one will too.

But here is the part most analyses skip: the democracies are starting to draw lines through this market, and the lines are investable. This month, the CEO of one of the leading AI labs published a policy framework calling for fully autonomous weapons to be banned from domestic law enforcement, hardwired to refuse unlawful orders, and for the data-broker loophole that feeds bulk surveillance to be closed. Proposals like that are moving from think pieces toward statute. If they land, the market bifurcates by jurisdiction: domestic deployment constrained by constitutional guardrails, allied and export demand far less so. The companies that can build persistent autonomy for the coalition’s edge while staying inside the guardrails at home will capture both sides of the split.

Do not make the mistake of reading the guardrails as a tax on the thesis. They are what makes the Western stack durable. A security architecture that requires repressing its own population is brittle; it manufactures its own backlash. Legitimacy is a strategic asset too, and it is the one asset the other bloc cannot copy.

How the Market Misprices It

For markets, this is enormous.

The entire stack of frontier technology now operates inside a national security envelope, and the envelope tightens every year. Pricing companies inside this envelope as if they were ordinary consumer or enterprise software businesses is mispricing them. They are dual-use strategic assets in a fragmenting world, with all the upside and all the constraints that designation carries.

This is partly why the largest frontier companies have attracted capital at valuations that look insane to traditional analysts. The analysts are pricing commercial businesses; these are no longer commercial businesses. They are pieces of state capability with a commercial revenue line attached. Sometimes that makes the valuation more rational than it looks: a state backstop under the downside is worth turns of multiple that no spreadsheet captures. And sometimes the same designation is the warning: where the state owns the demand curve, you are holding the coupon, not the compounder.

You either build inside the National Security Stack, or you build around it. There is no neutral position anymore.

Alpha: the strategically protected category is the durable category, but only part of it compounds. Buy what governments will defend, subsidize, and onshore, where the market still sets the price.

IX. After Labor-Capitalism

Capitalism is finishing its job. The system that built modernity, the price-signal-and-property-rights coordination engine that bootstrapped humanity out of agricultural scarcity, is reaching the end of the phase it was designed to run. Not collapsing. Not failing. Completing.

What comes next is not socialism. It is a structural shift in which labor stops being the primary claim on output and ownership of automated production becomes the central economic question. That shift requires a new arrangement that nobody has fully built yet.

Every economic system humans have built is transitional. We tend to forget this because we live inside whichever one is current and assume it is the natural state of things. The peasants of medieval France assumed feudalism was eternal. The post-war managerial class assumed Keynesian capitalism was the end of history. Both were wrong. The transitions between systems are bloody and produce decades of cultural panic, but they also produce the largest expansions of human capability in recorded history.

We are roughly two and a half centuries into the capitalist era and visibly in its late stage. Capital is concentrated to historic extremes. Returns on labor have decoupled from returns on capital. Financial engineering dominates productive engineering as the path to wealth. The owners of capital have decoupled their fortunes from the welfare of the societies that produced them.

One thing to be precise about. I am not describing a moral collapse. I am describing a phase change. Capitalism did not become evil, and it is not being discarded. It is evolving. The price-signal engine that built modernity is entering its next phase, one where ownership of automated production becomes the central question rather than the sale of labor.

Capitalism’s core assumption is breaking: that human labor, applied through capital, produces wealth. Remove or massively diminish the labor input while making capital ten thousand times more productive through automation, and the mechanism that worked for two centuries starts to misfire. The richest companies in the world employ a fraction of the workers their predecessors did fifty years ago, while producing many multiples of the output. The wealth gap is not about whether the system is “fair.” The system was built for a labor-intensive environment, and we are entering a labor-light one.

The next system, whatever we end up calling it, will be organized around different questions. Capitalism asks: how do we coordinate human labor and capital to produce goods and services efficiently? The next system asks: how do we coordinate intelligence, agency, and abundant production to align outcomes with what is best for consciousness and civilization? Scarcity is no longer the central frame. Energy gets cheaper. Goods get cheaper. Even cognition gets cheaper. The bottleneck moves from “produce enough” to “decide what to produce, and how to distribute the output.”

Put it more directly. Every institution on Earth was built to coordinate scarcity. Nation-states, corporations, markets, legal systems, education, religion. All ten thousand years of civilization is downstream of the question “how do we allocate too few resources among too many wants?” That question is the operating system humans have been running. We are about to need a rewrite. The early kernel updates are already deploying. The full migration will take decades.

I am not predicting socialism. Socialism failed because it did not solve the coordination problem capitalism solved. The next system will not be socialism, and it will not be a managed economy. It probably does not have a name yet. What it will have to do is give citizens a claim on automated productivity, and price the things capitalism has been bad at pricing: long-term well-being, ecosystem health, civilizational coherence, the stability of the social fabric.

The Ownership Paths

The standard answer to mass automation is Universal Basic Income. Send everyone a check. Pay it out of taxes on the productivity of the machines. I understand why people reach for it. If labor income weakens, direct income replacement is the obvious first policy reflex.

But UBI has a structural weakness. It makes citizens dependent on the political system for a recurring transfer while leaving ownership of the productive base concentrated elsewhere. It can reduce suffering, but it does not solve alignment. It creates recipients, not participants.

The cleaner question is not “how do we send everyone a check?” The cleaner question is: how do citizens participate in the productivity of a civilization that increasingly produces output through capital, software, robots, energy systems, and automated infrastructure rather than through human labor?

There are several possible paths.

One is direct transfers: UBI, wage subsidies, tax credits, negative income taxes, emergency checks. These are politically simple and will almost certainly appear first. They are also fragile, because they remain dependent on annual politics and fiscal capacity.

Another is radical abundance. If AI, robotics, and energy drive the marginal cost of many goods and services low enough, the need for cash compensation declines. This is the most optimistic path, and parts of it are real. But abundance does not arrive evenly. Housing, land, healthcare, status, safety, and access to elite systems will remain scarce long after many digital goods become cheap.

Another is broad citizen ownership. This could mean sovereign wealth funds, birthright investment accounts, public equity stakes in strategic sectors, tax-advantaged citizen portfolios, or tokenized national equity. Universal Basic Equity is one version of this: every citizen receives some baseline ownership stake in the productive base of the society they belong to.

I do not mean equal equity. I do not mean equal outcomes. I do not mean flattening private wealth, punishing founders, or capping the upside of people who build. I mean a baseline civic stake. The point is not that everyone owns the same amount of the future. The point is that every citizen owns some amount of it.

The general idea is not mine. Citizen-owned equity in productive assets has been proposed in various forms by Yanis Varoufakis, Matt Bruenig, Marshall Steinbaum, and others. The Alaska Permanent Fund has delivered dividends from oil revenue since 1982. Norway’s sovereign wealth fund operates on similar logic at national scale. Trump Accounts, created under federal law in 2025, are a partial early version of birth-year endowment logic.

What matters is the principle: a citizen who owns a stake in the productive base is a participant, not only a dependent. They are less likely to experience automation purely as a threat if some portion of the upside compounds on their behalf.

I am not dogmatic about the mechanism. Universal Basic Equity may be the right version. A sovereign wealth model may be cleaner. Birthright accounts may be more politically viable. Direct transfers may dominate for a long time before anything better appears. The form matters less than the direction: as labor’s share of output declines, a stable society needs some way to broaden participation in capital ownership.

The most likely intermediate outcome is uglier: patchwork welfare, emergency checks, corporate benefits, surveillance-heavy public order, and a thousand temporary programs pretending to be a system. That is what inertia produces. Whether anything cleaner emerges depends on whether policymakers can imagine ownership as a stability mechanism rather than merely redistribution.